On Jan 1, 2011 I posted these goals:

1) Have at least $2000 in my Emergency Fund

2) Have at least $5000 in the Wedding Fund *joint savings with fiancee

3) Have at least $7000 in RRSPs

4) Pay off Visa (for good, dammit!)

5) Have MasterCard down to at least $8000

6) Pay down Citi (no goal, because the interest is so high, but make regular monthly payments)

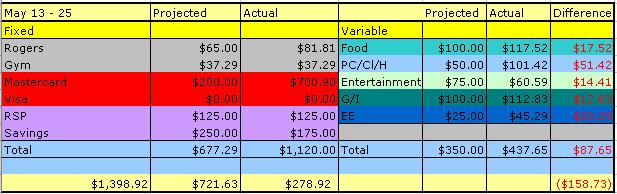

7) Not go over my budget more than $100 in any month

1) Right now its a

FAIL. If I was 25% done towards this goal my EF would be sitting at $500, its currently sitting at $411.52 (I had to take some money out to cover my glasses). However, I have increased my contribution to $200/mth. 9 months X $200/mth = $1800 plus $411.52 =

$2211.52 So, barring any major emergencies coming up between now and end of the year, I will still achieve this goal :)

2)

ON TRACK. Actually, we will probably be closer to $6000. Right now this account is sitting at $1980 with me contributing $150/mth and fiance will start contributing $300/mth starting in April (was contribution $100/mth but now that he's debt free! he is upping his contributions). So, $150 X 9 =$1350 plus $300 X 9 = $2700 =

$6030 plus interest :)

3)

ON TRACK. Currently sitting at $5470.66 I am making $250/mth contributions X 9 = $2250 =

$7720.66 I'm leaving the goal at $7000 because of market fluctuations. My RSPs are invested in mutual funds.

4)

DONE!!! Paid off Visa on March 17th and CLOSED IT on March 18th :)

5)

EXCEEDING When I wrote my goals I didn't know I was going to have this new job with the significant pay increase so I didn't know if I would be able to put big chunks on my debt. Well, my MasterCard is currently sitting at $8500 and I'm making $500/mth payments. $500 X 9 = $4500 = $4000 So I am now making this goal

$5000 to account for interest and maybe a month where I can't make the extra payment. Of course, I will still try my hardest to exceed this goal :)

6)

ON TRACK Well, since there was no goal per se on this one, I'm going to say I'm on track. Also, I made a $1098 extra payment in March and I am planning on throwing any extra money I make this year on this sucker (overtime, GST, surveys). I think I will now make the goal for this loan to be

$5000 too.

7)

COMPLETE and UDDER FAIL!!! I don't know why I put that as a goal, I should've known that there would be no way I could keep that. January I was over by $546.89, February $256.59; March $339.24!!! So, I don't know what I should do as a replacement goal. Or maybe I should just try harder? Now that I'm making more money and I've given myself more room for variable spending, maybe this is a possibility? Let's see at mid-year review :(

So, not too bad, 2 fails out of 7 but the first should actually not be a fail by the end of the year. I'm fairly content with this. I'm thinking next year I should add in no spend day goals and personal goals too. I may add them in starting mid-year. We'll see.

TTFN, Morgaine.

BTW, how are your yearly goals going so far? Are you on track?